We are pleased to share Karissa McDonough’s first Investment Thoughts as Chief Investment Officer. Karissa’s approach reinforces our long‑standing investment philosophy—focused on thoughtful diversification, risk management, liquidity, and building resilient portfolios through changing market conditions.

Global conflict combined with recent developments in private credit matter because these factors directly influence risk, liquidity, and how portfolios behave during periods of stress. In this Investment Thoughts we will share some thoughts on the outlook for both.

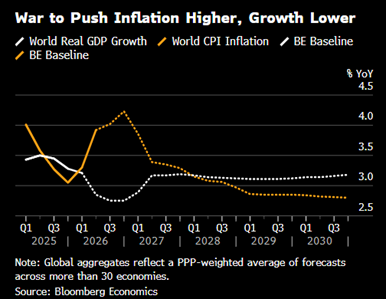

The chart below demonstrates the negative impact this conflict is having on multiple economic levers - both on growth as well as inflations over the course of next year.

Day-to-day headlines regarding either the extension of or breaking of the ceasefire has had the general impact of a significant rally or selloff in the stock markets. Similar dynamics are playing out in fixed income – with interest rates jumping with renewed tension/prolonging of the blockade. Given the news flow, investors are struggling to reconcile short-term market moves with possible lasting longer-term impacts on the economy.

As of April 27th, the ceasefire has been indefinitely extended as negotiations are ongoing. We continue to monitor developments in the conflict but reiterate our points from our previous Investment Thoughts:

Our philosophy has always been to mitigate risk to client portfolios from multiple angles – economic, inflation and interest rate risk. We have looked to provide an additional means of protection in portfolios in the form of Marketable Alternatives. Marketable Alternatives are comprised primarily of real assets—such as infrastructure, commodities, and real estate— which serve as natural hedges during periods of geopolitical tension or inflation pressure. These are considered marketable because held within mutual funds or ETFs that provide daily liquidity. Such assets have been helpful during this period of uncertainty, as they provide a stable source of income return with less attendant market volatility.

While the war in Iran continues to dominate headlines, it is not the only area demanding our attention. Separate from geopolitical developments, we are closely monitoring increasing scrutiny within private credit, where recent coverage has raised important questions around liquidity, valuation, and transparency. Capital markets participants have taken note of the exponential growth in the private credit market even as asset redemptions accelerate from this market.

Ledyard does not directly invest in private credit in client portfolios. While we studied private credit carefully as a potential investment, we ultimately decided not to invest in this area because we were concerned about the quality of some loans being made and the limited ability to get money out quickly if markets change—risks that could impact long‑term results.

Private Credit is a catchall phrase that primarily references lending done by Business Development Companies (BDC) which are non-bank financial institutions. This was a legal structure created in the 1980s to finance middle market US companies primarily to encourage venture capital but now serves as a proxy for the private credit industry. Total outstanding private asset investments across the financial system is close to $3T today.

In providing loans to companies that have fewer financing options, these firms act as middlemen and spread credit risk throughout the financial system. That means both banks that lend to them and investors in private credit funds share the risk if borrowers struggle.

Additionally, there are unique risks specific to private credit which are exacerbated when trends turn against borrowers in this space and defaults start to occur.

Weaker Balance Sheets. Unlike banks, which are required to set aside higher levels of capital on their balance sheets to protect the lender, depositors and the broader financial system from loan losses, NBLIs are not subject to similar requirements.

Asset/Liability Mismatch. Unlike banks, which benefit from FDIC backing of deposits and therefore have access to relatively stable long-term sources of cost-effective funding, BDCs have raised capital for their lending activities primarily from investors who have a much shorter investment time horizon than the terms of the loans they are funding.

This is why these funds have restrictions on investor withdrawals [also known as “gates”], because the funding model can’t withstand sustained outflows. This is what has been happening however, given the loss of confidence in the AI-impacted software industry which represents an outsized exposure of the BDC lending channel.

Private Credit not a Subprime Mortgage Scenario

The US banking system is strong at its core and average large bank lending to private credit is well below that of subprime RMBS in 2007/08. The current selloff in Private Credit reflects the riskier way capital was raised in this space, rather than a sudden deterioration in fundamentals.

The current backdrop for investors may feel more unsettled than usual. Investors face the combination of constant geopolitical headlines and uncertainty with respect to how the US economy will be impacted, plus evolving conditions with the financial system here at home.

The fundamental backdrop to the global capital markets remains healthy. Earnings growth for US companies are solid and thus far, GDP is likely to remain positive in 2026. Our investment process focuses on buying quality cash flows at reasonable valuations regardless of current events.

Periods like this reinforce the value of a disciplined, long-term approach focused on quality and resilience rather than market timing.

We are here to help. Please contact your wealth‑management team with any questions or if you would like to discuss your portfolios in greater detail. Our contact information is listed below.

Karissa McDonough, CFA

Chief Investment Officer

Office Phone: 603.640.2687

Karissa.McDonough@ledyard.bank